100%

Tax Mitigation

Overview

This is an opportunity to reduce your taxable income by up to $375,000 with a one-time $100,000 investment into an income-producing tiny home. This is a proven and well established tax strategy used by taxpayers just like you looking for an a tax deductible investments just like this.

Summary

Tax Investor Programs welcomes you to learn about this extremely valuable tax benefit associated with the Tiny Vacation Home, which qualifies as a business property under the Internal Revenue Code (IRC Section 179).

As per IRC Section 179, the Tiny Vacation Home is eligible for a 100% deduction in the first year of service. For tax years beginning in 2024, the maximum allowable deduction under this provision is $1,220,000. Additionally, larger deductions may be available under IRC Section 168(k), allowing for bonus depreciation benefits.

For example, if a taxpayer makes a one-time down payment of $100,000 toward the purchase of a tiny home, the remaining balance of $275,000 per unit can be structured as a cashflow buyout lease. This means that the remaining payments are covered by future cash flow, optimizing both tax and financial planning strategies.

Imagine not only owning a profitable and successful AIR BNB and also be able to deduct the entire expense from your budget.

Should you have any questions or require further clarification, please do not hesitate to reach out. I would be happy to discuss how this tax incentive could benefit your investment strategy.

Here is how it works.

1. One-Time Down Payment

With a one-time down payment of $100,000, the taxpayer acquires ownership of a Tiny House for $375,000.

2. Lease Agreement

Tax Investor programs manufactures and sells the tiny home on payment terms described above and keeps a security interest until the final payment is made.

Section 179

The amount of expense write off available in 2024 & 2025 is 100% of the basis of the asset placed into service in 2024. While real estate is not eligible under section 179, IRS rulings have concluded that when a structure is movable (such as with a wheeled trailer or tiny house) these portable homes are delivered on wheels and can be readily transported, and are therefore considered business property, not real estate.

A taxpayer puts a one-time $100,000 down payment toward the purchase of a tiny home, which is subject to a cashflow buyout lease with a remaining $275,000 per unit payable out of future cash flow.

Expense Write-off

Section 179 is a deduction that allows the tax payer investor to write off the cost of a qualified property or equipment as an expense, during the first year it was purchased and placed into service. Compared to section 168, which tax payers use to write-off a portion of the depreciation over 5 years, section 179 gives the tax payer the ability to deduct the entire cost in a single year.

A taxpayer puts a one-time $100,000 down payment toward the purchase of a tiny home, which is subject to a cashflow buyout lease with a remaining $275,000 per unit payable out of future cash flow.

Frequently Asked Questions

What Is Section 179?

Section 179 of the U.S. internal revenue code is an immediate expense deduction that business owners can take for purchases of depreciable business equipment instead of capitalizing and depreciating the asset over time.

What is the maximum deduction?

The maximum Section 179 deductions a tax payer can claim in 2024 tax year $1,220,000.

What does placed into service mean and when is the deadline?

Typical Tiny House Scenario

Edward is a skilled surgeon. At 56 years old, Edward is seeking ways to optimize his financial situation and reduce his tax liability. Let’s explore how he can leverage the Tax Investor Tiny House Program program to his advantage.

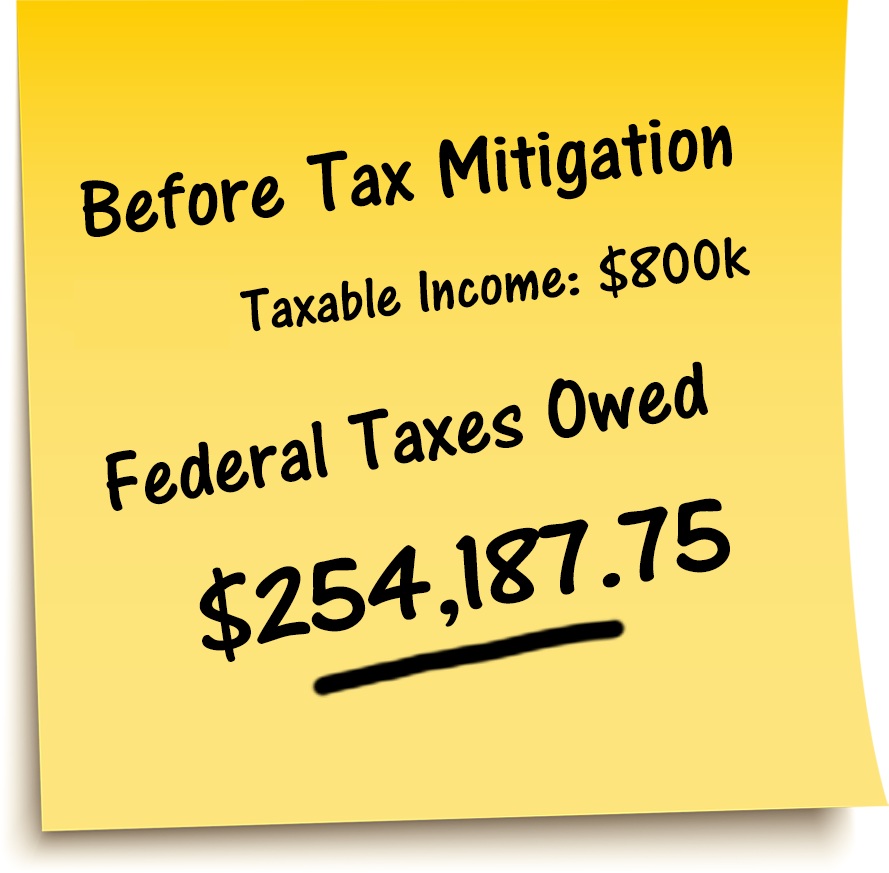

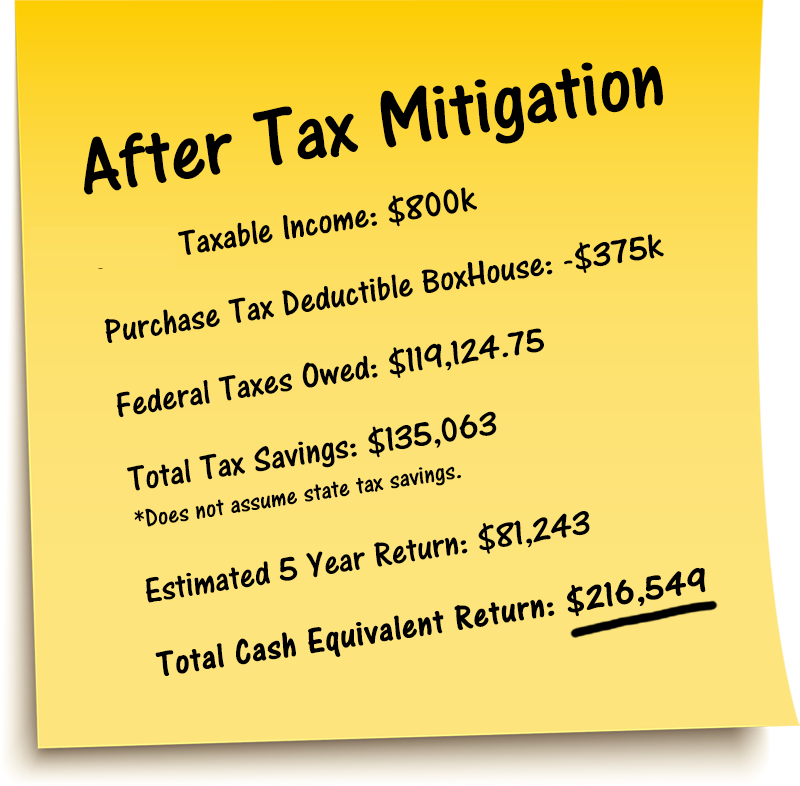

Edwards’s annual income as a surgeon stands at $800,000. Edward currently has a tax rate of 37% and is now subject to a tax obligation of $254,187. Edward would like to reduce his tax obligation. He is now the perfect candidate for the Tax Investor Tiny House Tax Mitigation program.

Let’s illustrate the specifics of Edwards’s tax-saving plan using Section 179 of the US tax code.

Edwards plans to purchase a Tiny House for $375,000. To secure the home, a purchase agreement is completed wherein Edward provides a down payment of $100,000.

The balance now owed is $275,000. This acquisition comes with a lease in place to a qualified lessee who places an end user in the home. The lessee agrees to pay the remaining $275,000 owed under the financing terms over 360 months. With the lease in place John does not need to worry about making the payments.

Now, due to the unique qualifications of a Tiny House Edward is able to deduct 100% of his tiny-home purchase in the first year by applying section 179 of the US tax code.

This unique purchase combination provides Edward with a substantial deduction which decreases his tax obligation.

Here is an example of how Edward’s tax obligation can be reduced by purchasing a Tax Investor Tiny House using Section 179.

*Edward is a single filer

One-Time Where are the tiny-homes installed?

The majority of homes are currently being installed in Tennessee.

Why Tennessee? Housing has been a major challenge for oil companies to secure in rural areas. The typical living situation for an oil field worker includes numerous employees sharing small confined spaces referred to as “Man Camps.” Companies in Tennessee are seeing the value in providing premium housing for their employees, where the alternative is an unappealing “man camp” that struggles to recruit and retain valuable employees. As evidenced by the photos below, Tennessee companies have been able to utilize the Tax Investor Tiny House to set themselves apart from others by providing far more appealing living accommodations.

About The Tiny House

Measuring 19 feet by 20 feet, or approximately 380 square feet, the Tax Investor Tiny House is designed to provide privacy and comfort by including a full kitchen, bathroom, bedroom, dining & living area.

Constructed with a steel frame and walls, the Tiny House is designed to endure significantly longer than conventional stick-built houses due to its reduced susceptibility to severe weather conditions, mold, rot, etc.

Man Camps

As you can see, the accommodations are much nicer in a Tiny as compared to typical “Man Camps” in Tennessee.

{kind=link}

{kind=link}

{kind=link}

Frequently Asked Questions

Who is responsible for vacancy, loss, or damage?

Who are the lessees and why do they want a Tiny House?

What are the total cash outlays?

How do I get started?

Is this a security?

References

1. Basis is the amount of your capital investment in property for tax purposes. Use your basis to figure depreciation, amortization, depletion, casualty losses, and any gain or loss on the sale, exchange, or other disposition of the property. The basis of an asset is its cost to you. The cost is the amount you pay for it in cash, debt obligations, and other property or services. See https://www.irs.gov/taxtopics

2. Borrowed cash is full basis, untaxed money in the borrower’s hands. These funds may be used to purchase assets with a full-cost basis that enables the financier to earn profits and suffer losses in operating or disposing of the assets. If the debt is genuine and reasonable in terms of the fair market value of the purchased property, the full amount of borrowed funds generally gives rise to cost basis.

3. There is no need to discount a note receivable to the present value when determining tax basis. See Peracchi, Donald J. et ux v. Commissioner where a 10-year note at 11% interest was held to contribute the full face value to the calculation of basis.

4. See Uniform Commercial Code §1-203. Lease Distinguished from Security Interest.

a. Whether a transaction in the form of a lease creates a lease or security interest is determined by the facts of each case.

b. A transaction in the form of a lease creates a security interest if the consideration that the lessee is to pay the lessor for the right to possession and use of the goods is an obligation for the term of the lease and is not subject to termination by the lessee, and: (1) the original term of the lease is equal to or greater than the remaining economic life of the goods; (2) the lessee is bound to renew the lease for the remaining economic life of the goods or is bound to become the owner of the goods; (3) the lessee has an option to renew the lease for the remaining economic life of the goods for no additional consideration or for nominal additional consideration upon compliance with the lease agreement; or (4) the lessee has an option to become the owner of the goods for no additional consideration or for nominal additional consideration upon compliance with the lease agreement.

5. This is based on our suggested use/exit. As the direct owner and manager of this equipment, the financier can modify the program to include renegotiating the buyout lease or any other element of the program. Nothing herein is intended to constitute a security nor to suggest that the financier is in any way a passive party to the transaction. Each transaction is entered into on a stand-alone basis, and there is no pooling arrangement.